Healthcare professionals work tirelessly to provide exceptional patient care, yet many overlook a powerful tool for securing their financial future: the 403(b) retirement plan. Understanding the 403b max contribution 2024 limits enables medical practice employees, administrators, and healthcare providers to maximize their retirement savings while reducing current tax burdens. For organizations managing complex revenue cycles and staffing structures, optimizing retirement benefits becomes a strategic component of competitive compensation packages that attract and retain skilled professionals in an increasingly challenging healthcare landscape.

Understanding the 403b Max Contribution 2024 Framework

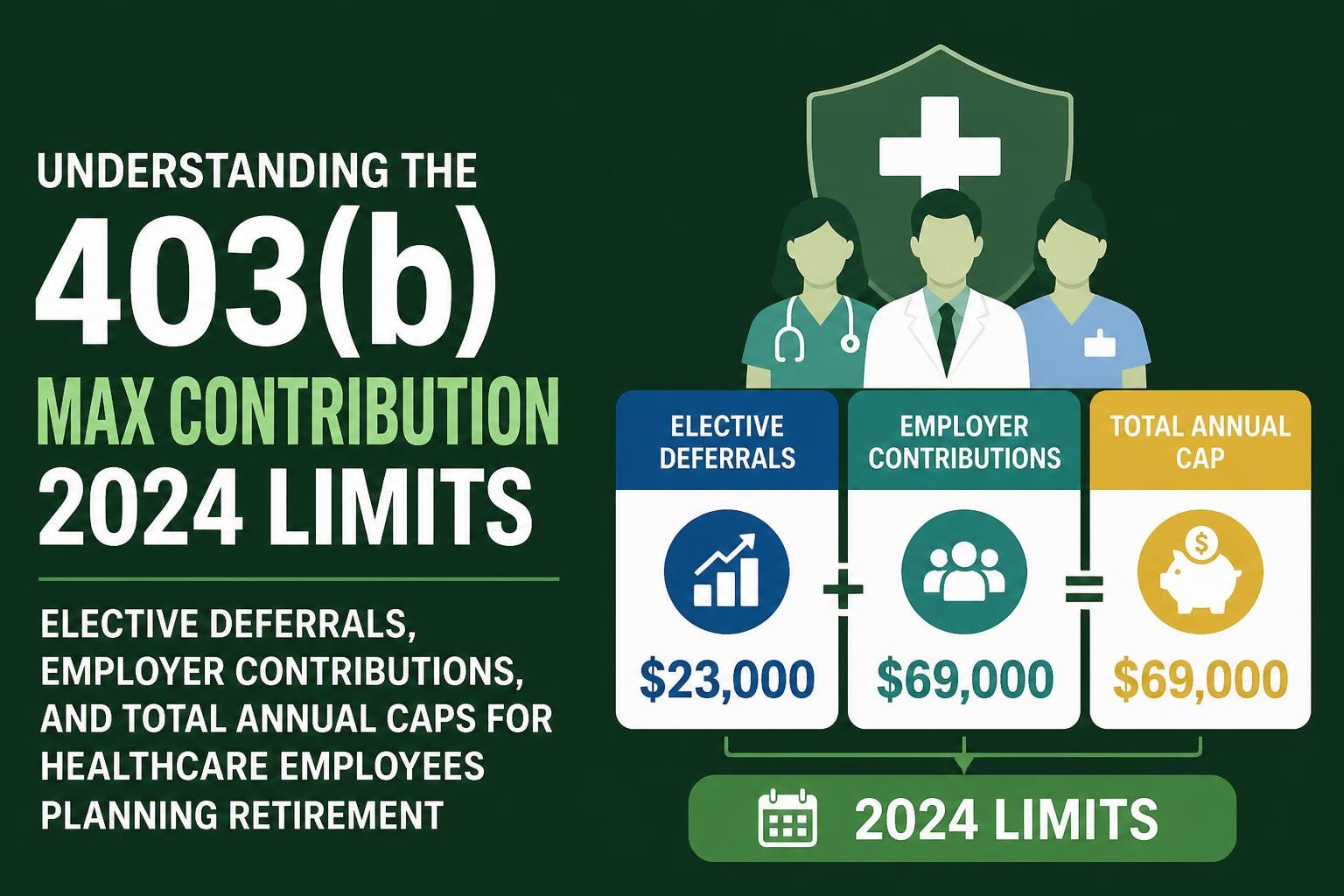

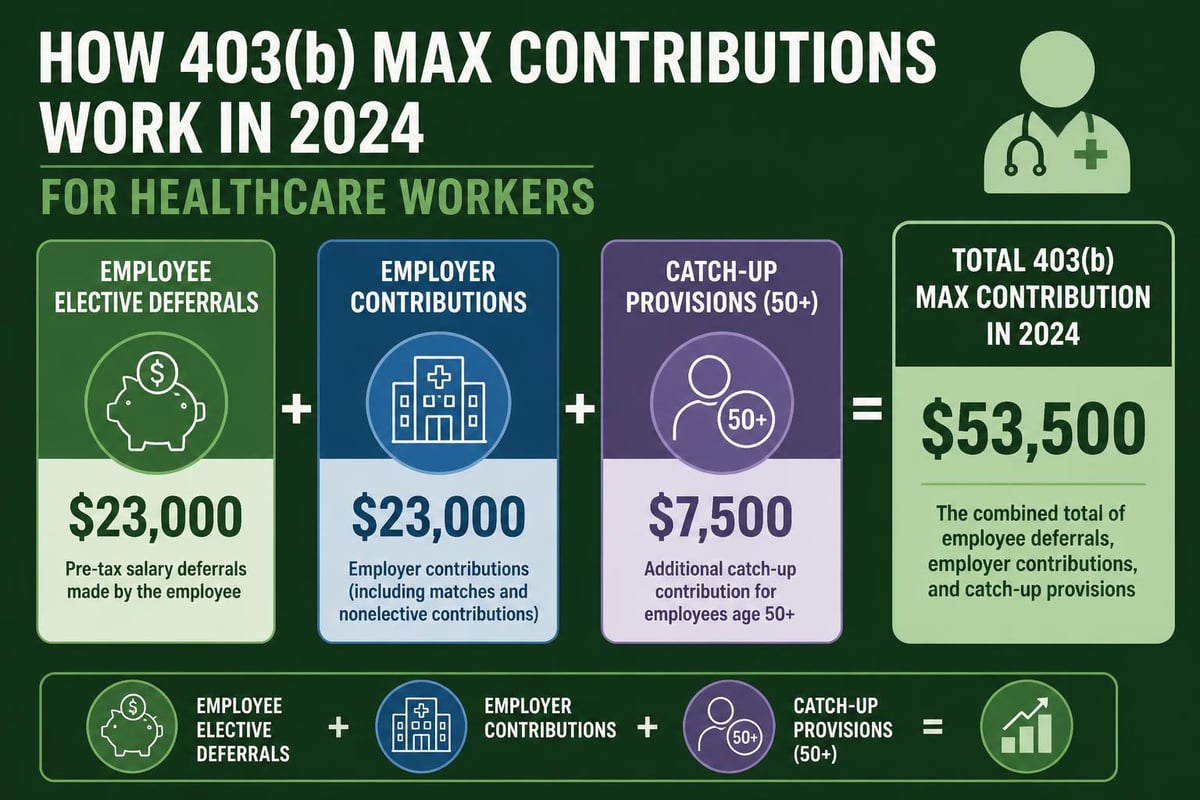

The 403b max contribution 2024 limits represent critical thresholds that healthcare employees and employers must navigate carefully. According to official IRS guidance on 403(b) contribution limits, the elective deferral limit for 2024 stands at $23,000 for most participants. This represents an increase from previous years, reflecting ongoing adjustments for inflation and cost-of-living considerations.

Total contribution limits extend beyond employee deferrals. When combining employee contributions, employer matches, and other allocations, the overall annual addition limit reaches $69,000 for 2024 or 100% of the employee's includible compensation, whichever is less. These combined limits create significant opportunities for healthcare organizations to structure comprehensive retirement benefits.

Employee Elective Deferrals

Healthcare employees can contribute up to $23,000 through salary reduction agreements. This amount represents pre-tax contributions that reduce current taxable income while building retirement wealth. For medical billing specialists, practice managers, clinical coordinators, and other healthcare professionals, maximizing this contribution provides substantial tax advantages.

Consider a healthcare administrator earning $85,000 annually who contributes the maximum $23,000. This reduces their taxable income to $62,000, potentially dropping them into a lower tax bracket while simultaneously building retirement assets. The immediate tax savings combined with tax-deferred growth creates a powerful wealth accumulation strategy.

Catch-Up Contribution Provisions for Experienced Healthcare Professionals

Healthcare professionals aged 50 and older benefit from additional contribution opportunities. The age 50+ catch-up provision allows an extra $7,500 in contributions beyond the standard 403b max contribution 2024 limit, bringing their total elective deferral capacity to $30,500.

Special 15-Year Service Rule

Uniquely among retirement plans, 403(b) arrangements offer a special catch-up provision for long-tenured employees. Healthcare workers with 15 years of service with qualifying employers may contribute an additional amount based on a complex calculation. The SHRM analysis of contribution limits highlights how this provision particularly benefits career healthcare professionals.

This 15-year rule allows up to $3,000 in additional contributions, subject to specific limitations:

- Maximum additional contribution: $3,000 per year

- Lifetime maximum: $15,000 total

- Calculation considers previous contributions and compensation history

- Cannot be combined with age 50+ catch-up in the same contribution category

| Contribution Type | Standard Limit | Age 50+ Addition | Potential Total |

|---|---|---|---|

| Elective Deferral | $23,000 | $7,500 | $30,500 |

| With Employer Match | Varies | Varies | Up to $69,000 |

| 15-Year Service (separate) | $3,000/year | N/A | $15,000 lifetime |

Healthcare organizations should integrate these contribution options into comprehensive health insurance management and benefits planning strategies.

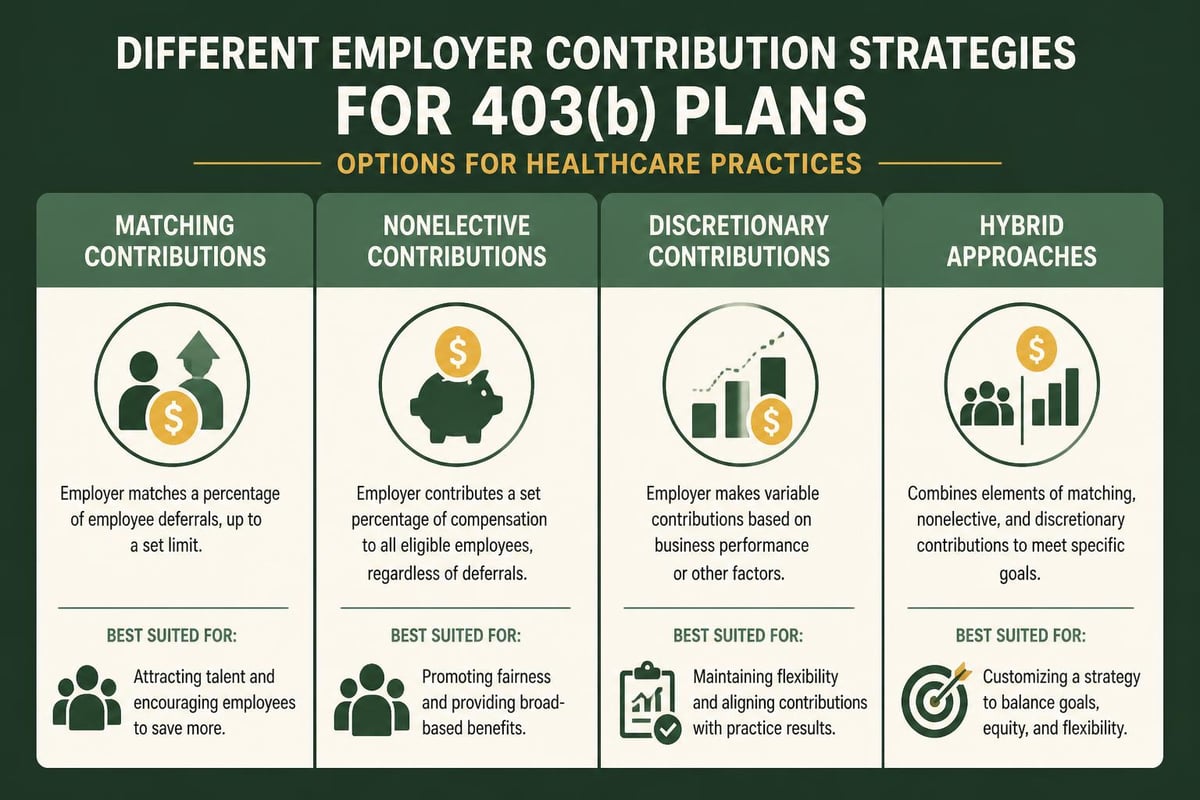

Employer Contribution Strategies for Healthcare Practices

Medical practices, hospitals, and healthcare organizations can significantly enhance retirement benefits through employer contributions. These contributions count toward the overall $69,000 limit but not the $23,000 elective deferral threshold, creating additional retirement funding opportunities.

Common employer contribution approaches include:

- Matching contributions: Employer matches employee deferrals up to a specified percentage (e.g., 50% of contributions up to 6% of salary)

- Nonelective contributions: Employer provides fixed percentage regardless of employee participation

- Discretionary contributions: Employer contributes variable amounts based on practice profitability

- Hybrid models: Combination of matching and nonelective contributions

For a medical practice utilizing comprehensive revenue cycle management services, optimizing cash flow enables more generous employer retirement contributions. When practices maximize reimbursements through effective denial management services and efficient claims processing, they create financial capacity for competitive benefits packages.

Compliance Considerations

The IRS 403(b) plan fix-it guide emphasizes the importance of monitoring total contributions. Healthcare organizations must implement systems ensuring combined contributions never exceed annual limits. Violations can result in:

- Excess contribution taxation to the employee

- Plan disqualification risks affecting all participants

- Correction procedures requiring administrative resources

- Potential penalties and interest charges

Strategic Planning for Healthcare Professionals

Maximizing the 403b max contribution 2024 limits requires intentional planning aligned with overall financial goals. Healthcare professionals should evaluate contribution strategies within the context of comprehensive financial planning.

Front-Loading Versus Spreading Contributions

Front-loading involves maximizing contributions early in the year, allowing more time for tax-deferred growth. This strategy proves particularly effective when:

- Healthcare professionals receive year-end bonuses

- Investment markets show positive momentum

- Cash flow allows aggressive saving

- Professionals anticipate mid-year income changes

Spreading contributions evenly throughout the year provides:

- Consistent dollar-cost averaging into investment markets

- Smoother impact on take-home pay

- Simplified budgeting and cash flow management

- Reduced risk of missing the contribution deadline

Coordinating Multiple Retirement Accounts

Many healthcare professionals maintain multiple retirement savings vehicles. Understanding how these interact prevents over-contribution while maximizing tax advantages. For example, healthcare workers with access to both 403(b) and 457(b) plans can maximize both, as they have separate contribution limits.

Consider this scenario:

A hospital administrator contributes $23,000 to their 403(b) plan and an additional $23,000 to a governmental 457(b) plan, totaling $46,000 in annual retirement savings. If aged 50+, they could add $7,500 to each plan, reaching $61,000 in total deferrals. This strategy dramatically accelerates retirement readiness for mid-career professionals.

Tax Implications and Roth 403b Options

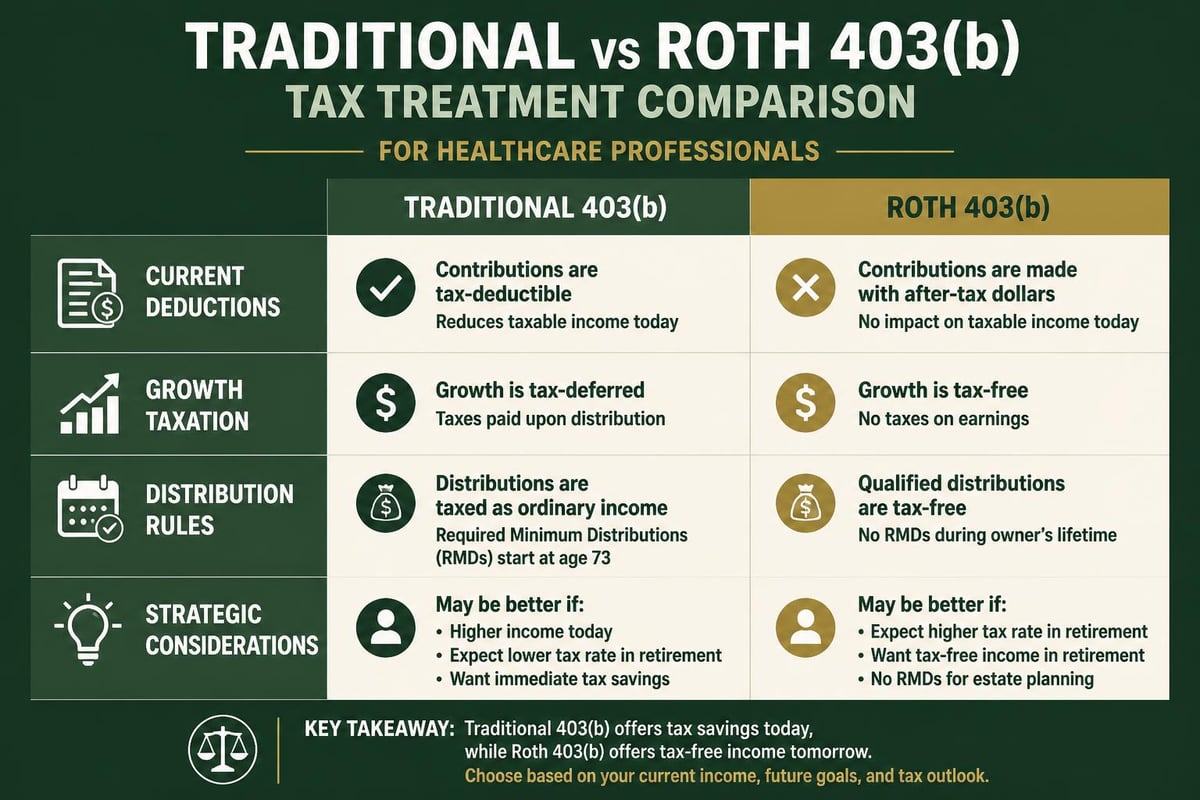

Understanding tax treatment optimizes the value of 403b max contribution 2024 allocations. Traditional 403(b) contributions reduce current taxable income, with taxation deferred until retirement distributions. However, many plans now offer Roth 403(b) options providing different tax treatment.

Traditional Versus Roth Contributions

| Feature | Traditional 403(b) | Roth 403(b) |

|---|---|---|

| Current Tax Treatment | Pre-tax (reduces taxable income) | After-tax (no current deduction) |

| Growth | Tax-deferred | Tax-free |

| Retirement Distributions | Fully taxable | Tax-free (if qualified) |

| RMDs Required | Yes, starting at age 73 | Yes, starting at age 73 |

| Income Limits | None | None |

Healthcare professionals in lower tax brackets early in their careers may benefit from Roth contributions, paying taxes at current lower rates while securing tax-free growth. Conversely, established practitioners in peak earning years typically prefer traditional pre-tax contributions to reduce current tax burdens.

Many experienced financial advisors recommend a hybrid approach, splitting contributions between traditional and Roth options. This strategy creates tax diversification in retirement, providing flexibility to manage taxable income when accessing retirement funds.

For healthcare practices managing their own financial operations alongside medical billing services, understanding these tax implications helps structure competitive employee benefits while managing organizational tax liability.

Implementation Best Practices for Healthcare Organizations

Healthcare practices implementing or optimizing 403(b) plans should follow structured approaches ensuring compliance, maximizing participation, and supporting employee retirement readiness.

Step-by-Step Implementation Guide

Step 1: Plan Design and Provider Selection

Evaluate 403(b) plan providers based on investment options, administrative services, fees, and participant education resources. Healthcare organizations should prioritize providers offering:

- Low-cost index fund options

- Comprehensive participant support

- Robust compliance monitoring

- Integration with payroll systems

- Clear fee disclosure

Step 2: Establish Contribution Policies

Define employer contribution formulas, vesting schedules, and eligibility requirements. Document these policies in formal plan documents and communicate clearly to all eligible employees.

Step 3: Implement Payroll Integration

Coordinate with payroll administrators to ensure accurate contribution processing. Systems must track employee deferrals, employer contributions, and cumulative totals against annual limits.

Step 4: Employee Education and Enrollment

Conduct comprehensive education sessions explaining the 403b max contribution 2024 limits, investment options, and enrollment procedures. Effective education significantly increases participation rates.

Step 5: Ongoing Compliance Monitoring

Establish quarterly review procedures ensuring contributions remain within legal limits, plan documents reflect current regulations, and all required testing and reporting occurs timely. Just as practices rely on comprehensive revenue cycle management for financial operations, retirement plan management requires systematic oversight.

Maximizing Employee Participation

Higher participation rates strengthen retirement security across the organization while demonstrating employer commitment to long-term employee welfare. Effective strategies include:

- Automatic enrollment: Defaulting new employees into the plan at a standard contribution rate

- Escalation features: Gradually increasing contribution rates annually

- Employer match visibility: Clearly communicating the value of employer contributions

- Financial wellness programs: Providing broader financial education beyond retirement planning

- Streamlined enrollment: Simplifying the sign-up process through digital platforms

Common Mistakes and How to Avoid Them

Healthcare professionals and organizations frequently encounter pitfalls when managing 403(b) contributions. Awareness of these issues enables proactive prevention.

Over-Contribution Errors

Problem: Employees exceeding the 403b max contribution 2024 limits through multiple employers or calculation errors.

Solution: Implement quarterly contribution monitoring. Employees with multiple healthcare employers must track combined contributions across all plans. Excess contributions must be withdrawn by April 15 of the following year to avoid double taxation.

Neglecting Catch-Up Provisions

Problem: Eligible employees aged 50+ failing to utilize the additional $7,500 catch-up contribution.

Solution: Proactively notify employees approaching age 50 about enhanced contribution opportunities. Automate catch-up contribution offers through enrollment systems.

Misunderstanding Employer Contribution Timing

Problem: Confusion about when employer contributions count toward annual limits.

Solution: Clarify that employer contributions are allocated based on the plan year to which they relate, not necessarily when deposited. This distinction affects year-end contribution planning.

Inadequate Investment Diversification

Problem: Concentrating 403(b) assets in single investment options or overly conservative allocations.

Solution: Provide access to target-date funds or managed account services. Encourage regular investment review and rebalancing aligned with retirement timelines. Similar to how healthcare practices benefit from partnering with specialists like top medical billing companies rather than handling complex billing internally, employees benefit from professional investment guidance.

Future-Proofing Retirement Strategy

The 403b max contribution 2024 limits represent current regulatory parameters, but successful retirement planning requires forward-looking perspective. Healthcare professionals should anticipate future adjustments and plan accordingly.

Contribution limits typically increase with inflation, though not every year. Between 2020 and 2024, elective deferral limits increased from $19,500 to $23,000, representing an 18% increase over four years. Healthcare professionals should plan for continued increases while maximizing current-year opportunities.

Long-term planning considerations include:

- Projecting retirement income needs based on desired lifestyle

- Calculating required savings rates to achieve retirement goals

- Balancing retirement contributions with other financial priorities

- Reviewing and adjusting contribution strategies annually

- Coordinating with professional financial advisors

Healthcare organizations investing in strong financial wellness programs demonstrate commitment to employee long-term success. When practices optimize their own financial performance through services like eligibility verification and payment posting services, they create capacity to support robust employee benefits including retirement plans.

The interconnection between organizational financial health and employee benefit quality underscores why healthcare practices increasingly partner with specialized service providers. Just as practices delegate complex medical coding services to experts, retirement plan administration often benefits from specialized expertise.

Understanding and maximizing the 403b max contribution 2024 limits represents a fundamental component of financial wellness for healthcare professionals. Whether you're a practice administrator structuring employee benefits, a medical billing specialist planning your retirement, or a healthcare provider balancing multiple financial priorities, optimizing 403(b) contributions creates lasting financial security. The combination of generous contribution limits, flexible catch-up provisions, and powerful tax advantages makes 403(b) plans invaluable tools for healthcare professionals committed to building retirement wealth while serving their communities with excellence.

Maximizing retirement contributions within the 403b max contribution 2024 framework requires the same attention to detail and systematic processes that drive successful healthcare revenue management. At Greenhive Billing Solutions, we understand that when healthcare practices optimize their financial operations through expert revenue cycle management, they create the financial capacity to offer competitive retirement benefits that attract and retain exceptional staff. Our comprehensive services-from claims processing and denial management to eligibility verification-help practices maximize reimbursements and improve cash flow, strengthening their ability to invest in long-term employee success. Discover how Greenhive Billing Solutions can enhance your practice's financial performance and support your broader organizational goals.